Global light vehicle production data through July 2026 shows output tracking across more than 50 automaker groups, 140 brands, and 1,400 models worldwide. The comprehensive analysis, authored by Jonathan Storey and Ian Henry for Automotive World, provides a detailed snapshot of manufacturing activity during the first seven months of the year.

This type of production monitoring matters because it reveals real-time capacity utilization, regional demand strength, and which manufacturers are gaining or losing ground in the market. Production figures directly correlate to sales pipelines, inventory levels, and automaker profitability. They also signal where capital investment is flowing and which vehicle segments are receiving manufacturing priority.

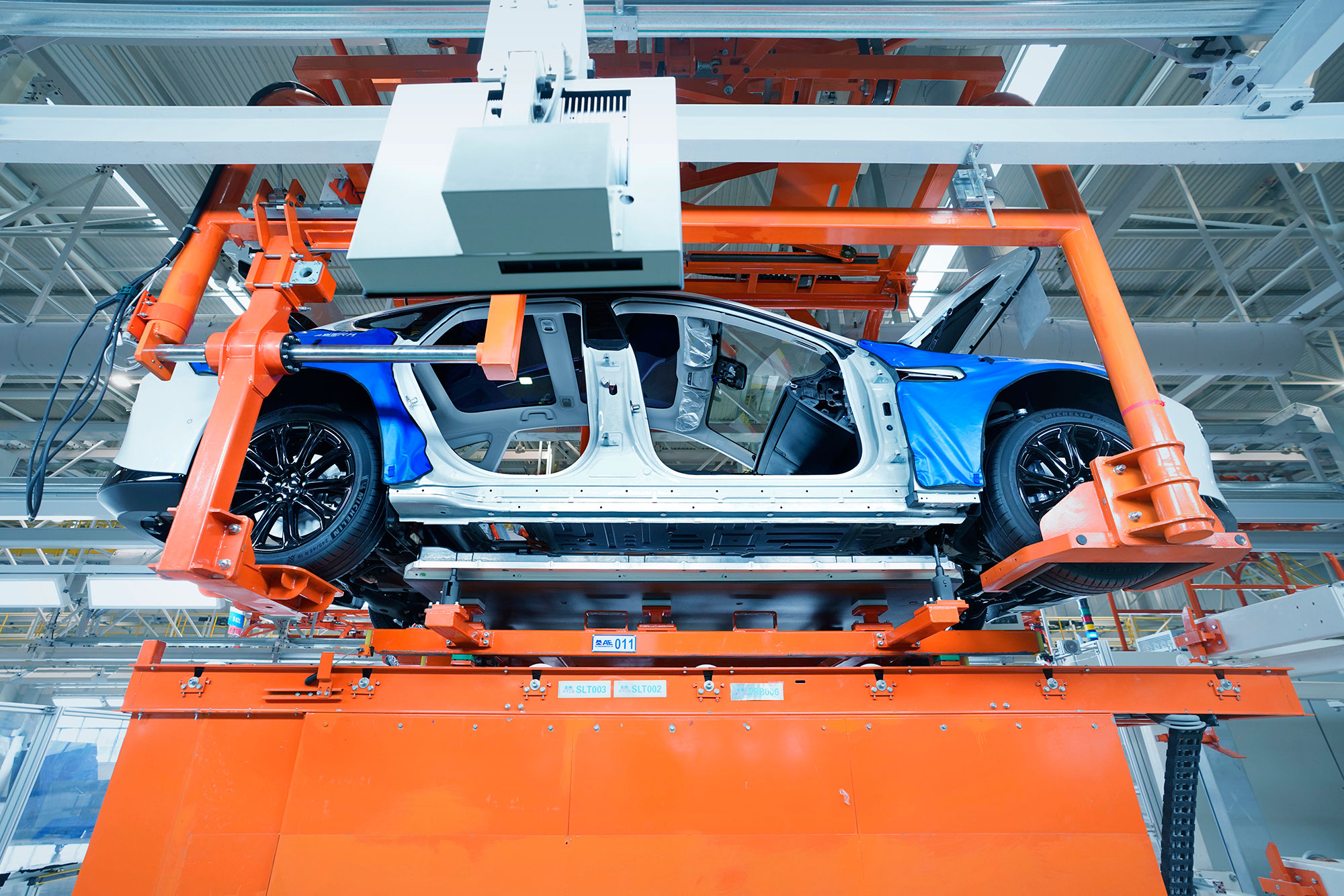

The July 2026 update captures a period when the industry faces competing pressures. Electric vehicle adoption continues reshaping assembly line requirements, with legacy automakers retooling plants alongside new EV-focused manufacturers ramping up output. Supply chain normalization post-pandemic has stabilized, but geopolitical tensions, tariff uncertainty, and raw material costs for battery production remain variables affecting production decisions.

Regional dynamics typically drive these numbers. Chinese manufacturers continue expanding capacity while Japanese and Korean producers optimize efficiency. European makers navigate stricter emissions regulations and EV transition timelines. American manufacturers manage the structural shift toward trucks and SUVs, which carry higher margins but require different platform architectures than sedans they previously built.

The breadth of this dataset—covering 50-plus automaker groups globally—provides visibility into whether the industry is operating near capacity or pulling back. Production velocity indicates confidence in dealer inventory levels and consumer demand forecasts. When automakers throttle production, it suggests demand softness or strategic inventory corrections. When they maximize output, it reflects confidence in sell-through rates.

For buyers and fleet managers, production data offers indirect signals about vehicle availability and potential pricing pressure. When specific models show constrained production, wait times extend and dealer